Financing Your Escape To The Country: Mortgages And Rural Property

Table of Contents

Understanding Rural Property Mortgages

Securing financing for rural property differs significantly from obtaining a mortgage for urban dwellings. While the dream of owning a country home is appealing, the reality of financing it requires a thorough understanding of the unique aspects of rural mortgages. Unlike urban mortgages, rural property financing often presents specific challenges related to appraisals, loan-to-value ratios (LTV), and property characteristics.

- Higher down payments may be required. Lenders often demand larger down payments for rural properties due to perceived higher risk, potentially requiring 20% or more of the purchase price.

- Stricter lending criteria might apply. Lenders may scrutinize your financial profile more rigorously, demanding higher credit scores and a more stable income history.

- Specialized lenders may be necessary. Not all lenders are comfortable with the complexities of rural property appraisals and the potential risks associated with these properties. You may need to seek out lenders specializing in agricultural or rural land loans.

- Access to reliable internet and utilities must be considered. The availability and cost of utilities (water, electricity, internet) can significantly impact a property's value and a lender's willingness to finance it. This needs to be factored into your appraisal and loan application.

Keywords: Rural mortgage rates, rural land loans, agricultural loans, country property financing

Finding the Right Lender for Rural Properties

Choosing the right lender is paramount when financing rural property. Your lender's experience and understanding of the unique aspects of rural land and properties will significantly impact your success.

- Research lenders specializing in agricultural or rural loans. Banks and credit unions may offer rural loans, but specialized lenders often have more experience and expertise in this niche market. This specialized knowledge is crucial in navigating the complexities of rural property appraisals.

- Compare interest rates and loan terms. Don't settle for the first offer you receive. Shop around and compare rates, fees, and loan terms from multiple lenders to secure the best possible financing.

- Consider the lender's experience with rural property appraisals. A lender's familiarity with rural property appraisals is critical. An accurate appraisal is vital for securing a fair loan amount.

- Look for lenders who understand the nuances of rural land ownership. Rural properties often present unique challenges, such as well and septic systems, that require a lender with specific knowledge.

Keywords: Best rural lenders, comparing mortgage lenders, rural loan specialists

Preparing Your Application for a Rural Property Mortgage

A strong financial profile and comprehensive documentation are essential for a successful rural property mortgage application. Preparing thoroughly will significantly increase your chances of approval.

- Improve your credit score before applying. A high credit score demonstrates financial responsibility and significantly improves your chances of loan approval, especially for rural properties where lenders may have higher risk assessments.

- Gather proof of income and assets. Prepare all necessary documentation, including tax returns, pay stubs, bank statements, and investment accounts, to demonstrate your financial stability and ability to repay the loan.

- Obtain a detailed property appraisal. A professional appraisal is crucial. It establishes the property's fair market value, which directly impacts the loan amount you can secure.

- Prepare for questions about your plans for the property. Lenders may ask about your intended use of the property. Be ready to clearly explain your plans and how you will maintain the property.

Keywords: Rural property application, mortgage pre-approval, improving credit score for mortgage

Unique Considerations for Rural Property Purchases

Rural property ownership comes with unique considerations that differ greatly from urban living. These factors significantly impact the overall cost and should be factored into your budget.

- Factor in the cost of well and septic maintenance. Unlike city properties with municipal water and sewer systems, rural properties often rely on wells and septic systems, requiring regular maintenance and potential repairs that can be costly.

- Research property taxes in the rural area. Property taxes vary widely by location. Understanding the tax burden of your chosen rural area is essential in your financial planning.

- Budget for potential repairs and renovations. Older rural properties may require significant repairs or renovations. Include a contingency fund to cover unforeseen expenses.

- Understand the implications of distance from urban services. Distance from hospitals, emergency services, and shopping centers can impact lifestyle and potentially increase insurance premiums.

Keywords: Rural property maintenance, country property taxes, rural property repairs

Exploring Alternative Financing Options

While traditional mortgages are the most common financing route, alternative options can be explored.

- Investigate seller financing options. The seller might be willing to finance a portion of the purchase, offering more flexibility.

- Research USDA rural development loans. The USDA offers various loan programs designed to support rural development, including financing for rural homes and properties. These programs often come with lower interest rates and more flexible terms.

- Explore state and local government programs. Some states and localities offer programs to encourage rural development and assist with homeownership.

Keywords: USDA rural development loans, seller financing rural property, alternative rural financing

Conclusion

Securing financing for rural property requires careful planning and choosing the right lender. Understanding the unique challenges and opportunities of rural mortgages is crucial for a successful purchase. Remember to meticulously prepare your application, thoroughly research lenders specializing in rural property financing, and factor in all associated costs, including property taxes and potential repairs.

Call to Action: Start your journey towards financing your dream escape to the country today! Research lenders specializing in rural property and begin preparing your application for a successful rural property mortgage. Don't let your dream of owning rural property slip away; take action and secure your future in the countryside.

Featured Posts

-

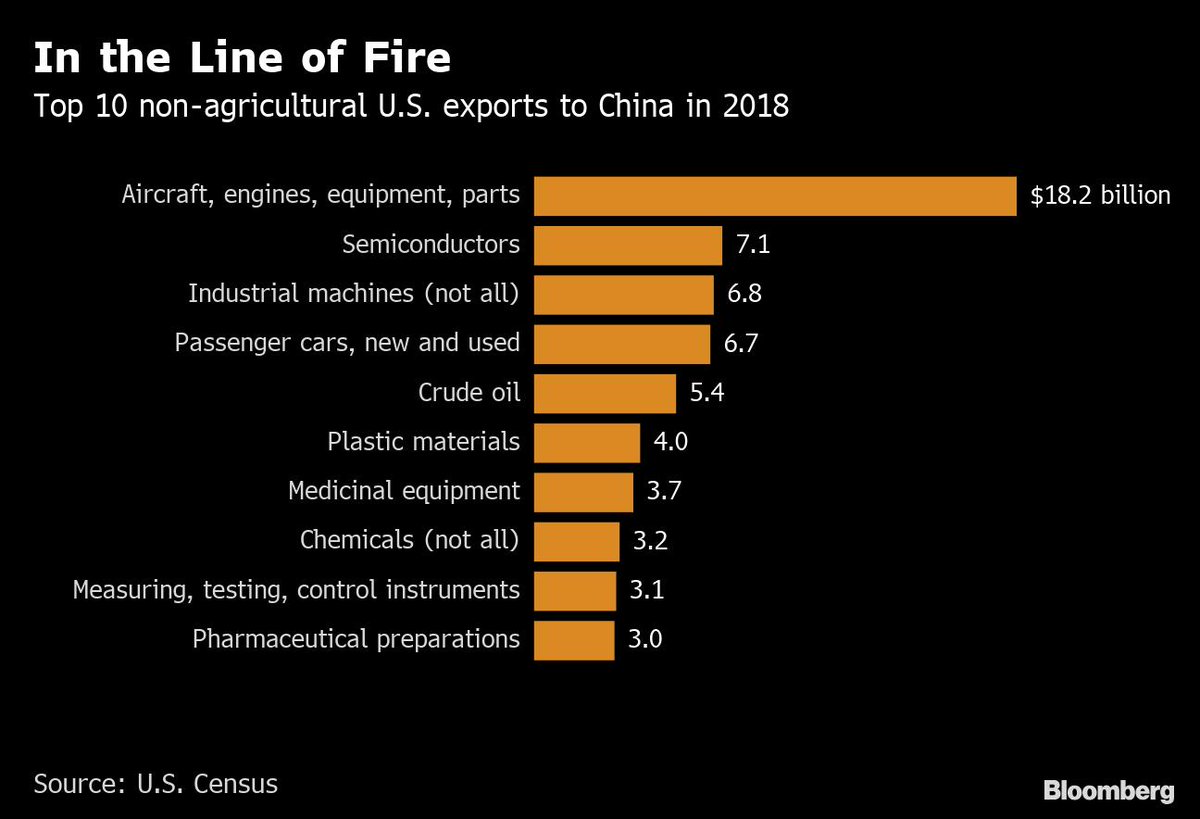

Atfaq Jmrky Amryky Syny Ydfe Mwshr Daks Ila 24 000 Nqtt

May 24, 2025

Atfaq Jmrky Amryky Syny Ydfe Mwshr Daks Ila 24 000 Nqtt

May 24, 2025 -

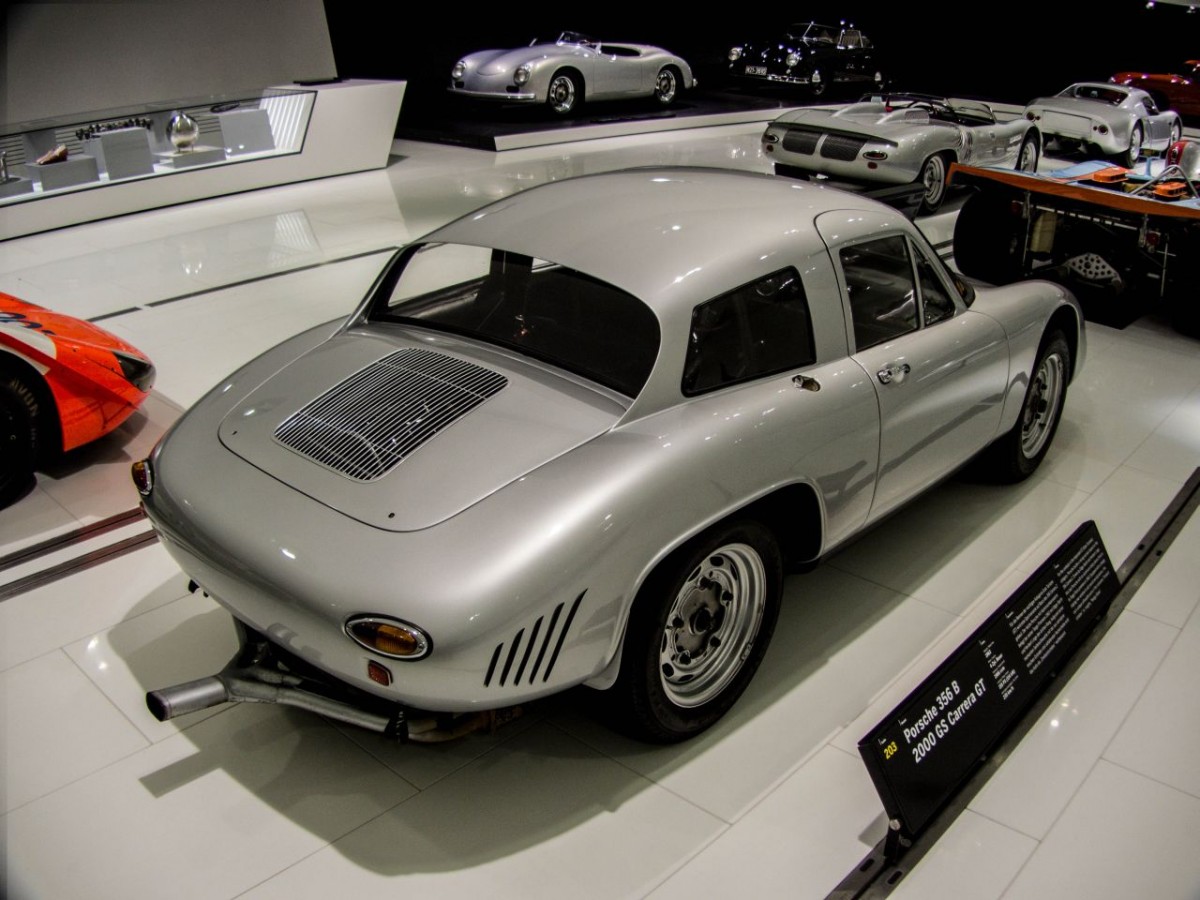

Porsche 356 Dari Zuffenhausen Ke Legenda Otomotif Jerman

May 24, 2025

Porsche 356 Dari Zuffenhausen Ke Legenda Otomotif Jerman

May 24, 2025 -

Walker Peters To Crystal Palace Free Transfer Speculation Mounts

May 24, 2025

Walker Peters To Crystal Palace Free Transfer Speculation Mounts

May 24, 2025 -

Amsterdam Stock Market Three Days Of Significant Declines Totaling 11

May 24, 2025

Amsterdam Stock Market Three Days Of Significant Declines Totaling 11

May 24, 2025 -

De Zaraz Peremozhtsi Yevrobachennya Ostannikh 10 Rokiv

May 24, 2025

De Zaraz Peremozhtsi Yevrobachennya Ostannikh 10 Rokiv

May 24, 2025

Latest Posts

-

The Iam Expat Fair Housing Finance Kids Activities And More

May 24, 2025

The Iam Expat Fair Housing Finance Kids Activities And More

May 24, 2025 -

Iam Expat Fair Your One Stop Shop For Housing Finance And Family Entertainment

May 24, 2025

Iam Expat Fair Your One Stop Shop For Housing Finance And Family Entertainment

May 24, 2025 -

Iam Expat Fair Housing Finance Fun And Kids Activities

May 24, 2025

Iam Expat Fair Housing Finance Fun And Kids Activities

May 24, 2025 -

Philips Convenes Annual General Meeting What Shareholders Need To Know

May 24, 2025

Philips Convenes Annual General Meeting What Shareholders Need To Know

May 24, 2025 -

2025 Philips Annual General Meeting Agenda And Important Updates

May 24, 2025

2025 Philips Annual General Meeting Agenda And Important Updates

May 24, 2025